We are entering unprecedented and perilous economic times. Today for the first time in history the price of West Texas Intermediate crude oil went negative, with the May delivery plunging to -$36.73 per barrel. Our fiscal policy makers are in panic mode as they try to stave off a deflationary spiral that could plunge the country into a deep depression. In this article I will discuss the government’s response to the current crisis, whether the law of unintended consequences will result in the destruction of the dollar, and possible replacements for the dollar as the world’s reserve currency.

The Government’s Plan

Even before the crash of the oil market, Fed policy makers knew deflationary pressures caused by the COVID-19 crisis were inevitable, and on March 15 the Fed lowered its target interest rate to near zero and announced a $700 billion quantitative easing (“QE”) program. And that’s just the beginning of the Fed’s plan to implement a stimulus plan that is breathtaking in its sheer never-before-imagined scope. On March 23, the Fed announced that it would continue its QE program on an “unlimited” basis. CNBC reports:

When everything is done, the Fed could have a balance sheet, consisting mainly of the bonds it has purchased to support markets and the economy, approaching $10 trillion, according to Krishna Guha, head of global policy and central bank strategy for Evercore ISI. ‘As things stand the Fed is racing very quickly towards a $7 trillion balance sheet and our best guesstimate is that it might peak in the very broad vicinity of $9 or $10 trillion,’ Guha said in a note to clients. ‘This is monetized credit policy and fiscal-monetary support on a grand scale.’

According to the article, the previous record high for the Fed’s balance sheet was $4.7 trillion, less than half of the $10 trillion balance sheet analysts expect before the end of the year.

In addition to the trillions of dollars in monetary stimulus, on the fiscal side Congress passed and President Trump signed a $2.2 Trillion dollar stimulus package on March 27. All of this will be funded by a massive increase in the federal debt. MarketWatch reports:

Investors are awaiting a flood of short-term debt issuance from the U.S. government after President Donald Trump signed off on a $2.2 trillion rescue stimulus package to soften the blow from the COVID-19 pandemic. Much of the borrowing used to finance the stimulus measures is expected to come from the market for Treasurys bills, or debt with maturities of a year or less, with some analysts anticipating more than $2 trillion of bill issuance in 2020 . . . Before the coronavirus outbreak, the U.S. was already headed for annual trillion-dollar fiscal deficits, but the recent stimulus package will accelerate the climb in government debt levels. A new study by Morgan Stanley estimates the deficit will total at least $3.7 trillion in calendar year 2020 and an additional $3 trillion in calendar year 2021. That suggests nearly $5 trillion in extra deficit spending in the next two years, financed by the sale of Treasurys.

Historical Perspective

As this chart shows, when George W. Bush took office in January 2001, the entire federal debt held by the public was $3.43 trillion. Think about that number. The deficit for the single year of 2020 will be more than the entire national debt was in 2001. At the end of 2019, the debt held by the public stood at $17.2 trillion. By the end of 2020, it is expected to exceed $20 trillion.

Source: St. Louis Fed.

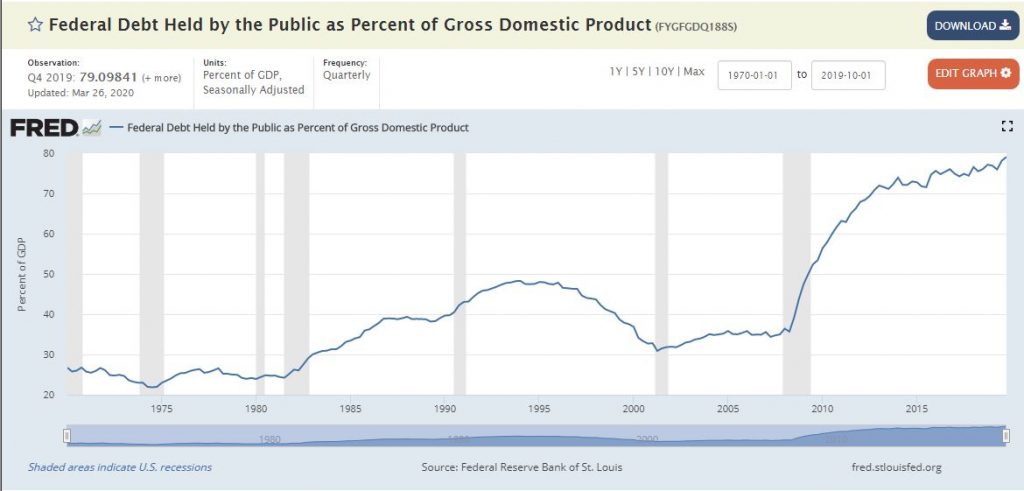

Not only is the federal debt growing at a mindboggling pace in absolute terms, it is growing rapidly in relative terms (as a percentage of GDP) as well. The next chart shows that when Bush took office in 2001, the federal debt was 32.8% of GDP. At the end of 2019, it was 79% of GDP. It is projected to approach 100% of GDP by the end of 2020.

Source. St. Louis Fed.

What Do the Fiscal Hawks Say?

Scott Wolla is the Economic Education Coordinator at the Federal Reserve Bank of St. Louis. In November 2019 – at a time when no one had ever heard of the coronavirus or COVID-19 – Wolla wrote a report for the Fed entitled Making Sense of the National Debt. Key passages from the report bear quoting at length.

The Government Accountability Office (GAO) suggests that the U.S government debt is currently on an unsustainable path: The federal debt is projected to grow at a faster rate than GDP for the foreseeable future. A significant portion of the growth in projected debt is to fund social programs such as Medicare and Social Security. Using debt held by the public (instead of total public debt), the debt-to-GDP ratio averaged 46 percent from 1946 to 2018 but reached 77 percent by the end of 2018 (see Figure 3). It is projected to exceed 100 percent within 20 years.

Notice that just last fall, the Fed was projecting that the national debt would exceed 100% of the GDP within 20 years. The current projection is that the debt will approach or exceed 100% of GDP within one year. The horizon has been narrowed by over 19 years in the course of just six months. And if government debt was on an unsustainable path in November, how much less sustainable is it now that we’ve added at least $2.2 trillion to the total in this year alone?

Back to Wolla’s report:

Economist Herb Stein once said, ‘If something cannot go on forever, it will stop.’ In other words, trends that are unsustainable will not continue because the economy will adjust, sometimes in abrupt and jarring ways. While governments never have to entirely pay off debt, there are debt levels that investors might perceive as unsustainable. A solution some countries with high levels of unsustainable debt have tried is printing money. In this scenario, the government borrows money by issuing bonds and then orders the central bank to buy those bonds by creating (printing) money. History has taught us, however, that this type of policy leads to extremely high rates of inflation (hyperinflation) and often ends in economic ruin. Some of the better-known examples of such polices are Germany in 1921-23, Zimbabwe in 2007-09, and Venezuela currently.

Focus on the printing money part. When it reported on Wolla’s report, CNBC wrote:

The Fed itself has come under criticism for “money printing,” which it did in three rounds of quantitative easing during and after the Great Recession. This came along with keeping its short-term lending rate anchored near zero for seven years.

This is a key point: QE is like printing money in the sense that it increases the money supply. There is no actual printing; it is all done through accounting entries in the Fed’s computer. Nevertheless, it is the 21st century equivalent of running the presses.

Is printing money through QE necessarily bad? No, just as printing money on a press was not necessarily bad in the good old days, printing money digitally is not necessarily bad today. Indeed, the Fed gets lots of credit for implementing QE to help the country out of the 2008 fiscal crisis. Printing money whether physically or digitally is not necessarily a bad thing. But there is a saying: “Pigs get fat; hogs get slaughtered.” Something that is good at one level can be disastrous at a higher level. Two aspirins will make your head feel better. A bottle of aspirin will kill you.

How much money printing is too much? Here is the concluding paragraph of Wolla’s report:

The national debt is high by historical standards—and rising. People often assume that governments must pay off their debts in the same way that individuals do. However, there are important differences: Governments (and their economies) do not retire, and governments do not die (or don’t intend to). As long as their debt payments remain sustainable, governments can finance their debt indefinitely. And if a government prints money to solve its debt problem, history warns that hyperinflation and financial ruin will likely result. While debt in itself is not a bad thing, it can become dangerous if it becomes unsustainable.

What do Fiscal Owls Say?

Enter the Owls. In recent years a school of thought known as Modern Monetary Theory has become increasingly popular especially among progressives such as Bernie Sanders and Alexandria Ocasio-Cortez. The basic tenet of MMT is that deficits don’t matter, because the government can just print more money to pay the interest on all of the debt that piles up. Another name for printing money to pay the debt is “monetizing the debt.”

As Wolla points out, historically governments that have monetized their debt succeeded in nothing but touching off hyperinflation. That is why Fed Chairman Jerome Powell described the idea as “wrong.” Powell’s comments seem somewhat ironic at a time when the Fed appears ready to step in and monetize up to $5 trillion of the federal debt. Even more ironic is that at this same hearing – which was before the Fed girded its loins to deal with COVID-19 – Powell echoed the GAO as quoted in Wolla’s report when he said that U.S. fiscal policy is “unsustainable.” If it was unsustainable before COVID-19, where is it now?

Summary of Our Current Situation

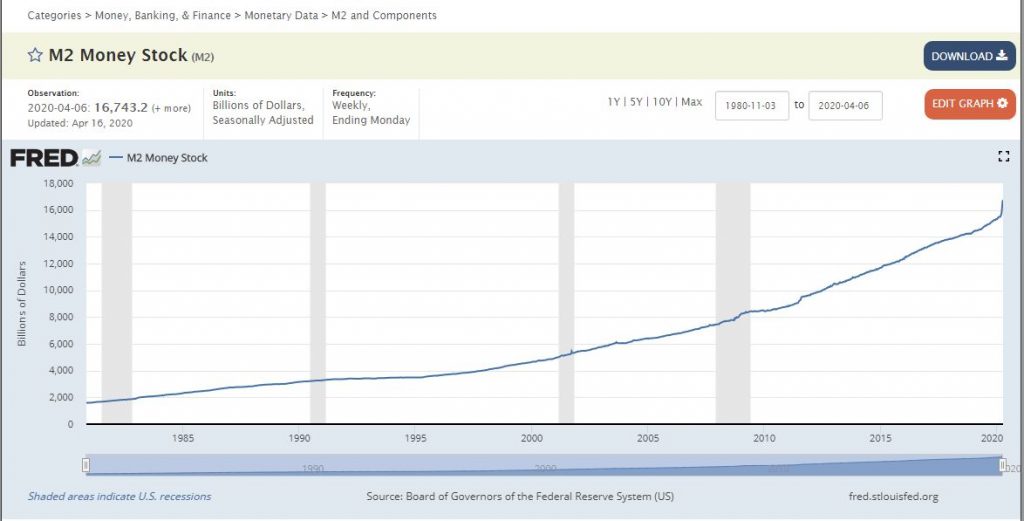

I am pessimistic about our current situation for two reasons, one monetary and the other fiscal. “M2” is a broad measure of money and money equivalents. The merest glance at a chart tracking M2 should ring klaxon alarms everywhere. When Bush took office in January 2001, M2 stood at $4.9 trillion. On January 13, 2020, M2 was $15.4 trillion. Just 70 days later, on March 23, 2020, M2 was $16.7 trillion.

Source: St. Louis Fed.

Notice how the curve starts to go almost straight up in 2020. And March 23 was only the beginning of the Fed’s monetary stimulus plan. It seems to me to be just plain common sense that if the increase in a nation’s money supply is represented by a near vertical line, that nation may soon reach a tipping point – the point at which there is so much money that the value of the money plummets and hyperinflation kicks in.

On the fiscal side of the equation, as described above, the Fed stated repeatedly BEFORE the COVID-19 crisis that our debt policies were unsustainable. How much more is this true now that an estimated $5 trillion dollars of debt is projected to be added onto an already unsustainable debt burden. Keep in mind that the debt burden is just the “on the books” debt. If one adds the unfunded liabilities from the government’s promises to fund Social Security, Medicare and other programs – which even under the most optimistic estimates constitute additional tens of trillions of dollars — the situation looks bleak indeed.

Government debt in itself is not a bad thing. QE in itself is not a bad thing. But if debt and QE are aspirins, it is becoming increasingly clear that the federal government has swallowed down a bottle full. Every reasonable person agreed that we were on an unsustainable path before the COVID-19 crisis. The additional fiscal and monetary burden caused by the crisis only exacerbates an already untenable situation. One cannot be blamed for wondering if we are near the tipping point.

Where Are We Heading?

Those are the facts. And those facts raise the question, where are we going from here? Predicting the economic future is a perilous pursuit. Therefore, I am not dogmatic about the conclusions I draw below. This analysis is tentative, even speculative. But is does seem to me that something like what I am about to describe is entirely possible.

The federal government responded to the 2008 crisis with a fiscal and monetary stimulus that is similar to the one it is currently implementing, just on a much smaller scale. The issue is this: Is the current response more of the same from which we can expect a similar outcome or is it something entirely different? Are we still merely pigs or have we reached the tipping point into hog territory?

I believe reasonable people of good will can differ about the answer to this question. The stimulus package had near unanimous support in Congress. Fed policy makers see their current unprecedented QE initiative as not just one option among many, but as practically mandatory to stave off a depression. I am not impugning the integrity or the motives of any of our leaders. They find themselves in an untenable, perhaps impossible, situation. They are between the Scylla of doing nothing or too little — and watching the economy slide into a deep depression — and the Charybdis of pumping massive amounts of money and debt into an already overburdened system — which risks touching off hyperinflation.

But the fact that fiscal and monetary stimulus policies are being implemented by people of good will acting in good faith does not alter the laws of economics in the least degree. From 1930 onward, President Hoover acted in perfect good faith as he tried everything he could think of to rescue the economy. Nothing he did stopped the nation from sliding into the worst depression in its history. I am also sure that the Minister of Finance of Germany’s Weimar Republic never dreamed that his actions would set in motion a spiral of hyperinflation that would cause a loaf of bread to increase in price from 160 Marks at the end of 1922 to 200 billion (yes “billion”) Marks in 1923. Once the tipping point was reached and hyperinflation kicked in, the process took on a life of its own.

We are faced with the double burden of a money supply increasing at a vertical rate and unsustainable levels of debt. I fear we may already be on an inevitable path to the tipping point. If that is true, hard times lie ahead. There will be economic adversity to a degree not seen since the 1930’s. And even more ominously, if the value of the dollar is destroyed, its 75-year reign as the world’s reserve currency will come to an end.

What Does it Mean that the Dollar is a “Reserve Currency”?

The following is from Wikipedia’s article on Reserve Currency:

A reserve currency (or anchor currency) is a foreign currency that is held in significant quantities by central banks or other monetary authorities as part of their foreign exchange reserves. The reserve currency can be used in international transactions, international investments and all aspects of the global economy. It is often considered a hard currency or safe-haven currency. The United Kingdom’s pound sterling was the primary reserve currency of much of the world in the 19th century and first half of the 20th century. However, by the end of the 20th century, the United States dollar was considered the world’s dominant reserve currency. The world’s need for dollars has allowed the United States government as well as Americans to borrow at lower costs, giving the United States an advantage in excess of $100 billion per year.

Since the end of World War II, the dollar has been the world’s dominant reserve currency. This means that people in other countries trust the American dollar more than they trust their own money. This is why the Federal Reserve Bank of Chicago estimates that 60 percent of all U.S. bills and almost 80 percent of all $100 bills are now overseas. For a number of reasons, including the the relative stability of the American political system and the enormous size of the U.S. economy, foreigners have sought out dollars as a stable store of value. Think about it. If you lived in Venezuela right now where the inflation rate has been as much as 53 million percent (you read that correctly), would you want to put your life savings in bolívares or dollars?

What Happens if the Dollar Crashes?

For nearly a century the dollar has been the world’s dominant reserve currency. As of 2019, there was no currency that was even remotely available as an alternative. Over 60% of the world’s currency reserves were in dollars. The Euro was in second place with 20%, followed by the Yen at 6%. If the dollar crashes in the near future and vanishes as a stable reserve of value, for a number of reasons that are beyond the scope of this post, there is no obvious choice to replace it. So what will happen if the dollar crashes?

Enter the Global Digital Currency

In August 2019 – on the very cusp of the COVID-19 crisis – Bank of England governor, Mark Carney gave a speech to a gathering of central bankers in Jackson Hole, Wyoming in which he called for the creation of a digital global currency to replace the dollar as the world’s reserve currency. The Guardian covered Carney’s speech:

[Carney] has challenged the dollar’s position as the world’s reserve currency, arguing that it could be replaced by a global digital alternative to end a savings glut that resulted in 10 years of low inflation and ultra-low interest rates.

Likening the move to the end of sterling’s command of international money markets 100 years ago, Carney said the dollar had reached a level of dominance that meant it was a barrier to a sustainable recovery.

He said a new digital currency backed by a large group of nations would unlock dollar funds that governments currently hoard as an insurance policy in uncertain times . . . A digital currency ‘could dampen the domineering influence of the US dollar on global trade’, Carney said in [his] speech . . . The Chinese currency, the renminbi, has been cited as an alternative to the dollar along with proposed digital currencies such as Facebook’s Libra. Carney said neither was in a position to take over from the dollar, but new technologies could allow for a global digital currency to challenge the US currency . . . Carney said: ‘Retail transactions are taking place increasingly online rather than on the high street, and through electronic payments over cash. ’ The most high-profile of these has been Libra, a new payments infrastructure based on an international stablecoin fully backed by reserve assets in a basket of currencies including the US dollar, the euro and sterling. It could be exchanged between users on messaging platforms and with participating retailers.

Even before the current crisis, the world’s finance ministers were discussing the replacement of the dollar by a global digital currency, either Libra or something similar. If the dollar evaporates as a stable store of value, expect world governments to leverage the opportunity to end nearly a century of currency hegemony by the U.S. dollar.

Goodbye Privacy

Paper currency transactions are invisible to the government, and they hate that. Which is why in recent years there have been increasing calls for elimination of high denomination notes. Lawrence Summers, former Treasury secretary and director of the National Economic Council in the White House, argued for abolishing $100 bills in a 2016 op-ed, citing elimination of crime as the main reason. In a Harvard research paper, former Standard Chartered bank chief executive Peter Sands argued “By eliminating high denomination, high value notes we would make life harder for those pursuing tax evasion, financial crime, terrorist finance and corruption.” The European Central Bank eliminated the 500 Euro note in 2016 for many of the reasons advanced by Summers and Sands. It is likely the government will also cite concerns about the spread of the coronavirus as a reason to eliminate literally filthy lucre.

The government wants to eliminate paper currency and drive all transactions to the digital world, where every transaction leaves a trace the government can follow. It should come as no surprise then that China, the world’s foremost surveillance state, is leading the way with the nuts and bolts of digital currency technology. Just today (April 20, 2020), the Wall Street Journal reported that China’s central bank is rolling out a digital currency across four cities as part of a pilot program, marking a milestone on the path toward the first electronic payment system by a major central bank with the goal of eliminating paper currency. The WSJ reports: “While it won’t boast the anonymity that bitcoin and other cryptocurrencies tout, China’s central bankers have vowed to protect users’ privacy.” How reassuring. There is one thing about which we can be absolutely certain: China’s central bankers are lying liars (a trait they share with China’s healthcare officials). When this system is fully implemented, they will have access to and be able to trace every single transaction in the entire nation. More ominously, there is nothing to prevent them from simply turning a person’s access to their money off. In the past a freeze on bank accounts could be evaded at least partially by using paper money for all transactions. When the government has the ability to turn off access to both bank accounts and the digital currency that has replaced paper money, it will have the power to completely eliminate a person’s ability to enter into any monetary transaction at all.

Conclusion

The U.S. has long been on an unsustainable path, both monetarily and fiscally. It is possible, perhaps even likely, that despite the best intentions of federal policy makers, the massive monetary and fiscal stimulus packages put in place by the Fed and Congress will result in the U.S. reaching the tipping point at which hyperinflation kicks in and the value of the dollar is destroyed. For nearly a century the dollar has been, by far, the world’s dominant reserve currency. If the dollar crashes that status will come to a screeching halt. There is no obvious national currency that can replace the dollar as the world’s reserve currency. But in recent months (even before the current crisis), the world’s central bankers have discussed creating a global digital reserve currency to replace the dollar. In the near future we may see the creation of such a currency, perhaps backed by a basket of national currencies and other financial assets. Finally, we will also likely see the elimination of paper money, which will be replaced by digital money such as that currently being tested in China.

After all of this has plays out, we may have a global digital currency used by everyone in the world. The governments of the world will be able to trace every monetary transaction. And they will also have the power to completely cut off a person’s access to his or her money and prevent them from entering into any sort of monetary transaction.